Source: King Ranch Institute for Ranch Management | June 4, 2019

By Rick Machen, Paul C. Genho Endowed Chair in Ranch Management: King Ranch Institute for Ranch Management

Those in the ranching community equate rainfall with grass growth and good cattle performance. So how could rainfall be depressing the cattle market?

It goes back to the age-old inverse relationship between corn and cattle prices – as corn goes up, feeder cattle prices trend downward.

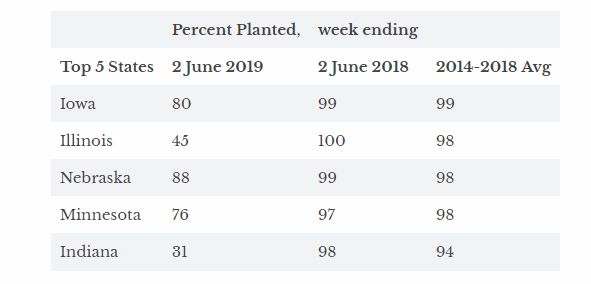

It is obvious that, due to unrelenting rain across much of the Corn Belt, a significant portion of the 2019 crop will be planted after May 30. For reference – research indicates the best time for Iowa farmers to plant corn is from April 20 to May 10. As planting date gets pushed back (see table), farmers will switch planting intentions and select shorter-season varieties of corn.

Interestingly, the corn plant has the ability to adapt to later planting by advancing more rapidly through the growth stages. Work done at Purdue and Ohio State indicates that the number of growing degree-days (GDD) needed from planting to maturity decreases by about seven GDD per day of delayed planting. For example, a hybrid planted on May 30 needs about 200 less GDDs to achieve maturity than a hybrid planted on May 1. Given this ability of the corn plant to adapt, the potential remains for a decent 2019 crop.

Once planted, yield will be influenced by growing conditions, namely temperature (being warmer than 86° F does not hasten growth but cool nights will slow accumulation of GDD), continued adequate soil moisture (timely late-season rain) and the (hopefully delayed) arrival of first frost. Farmers will be closely watching the cutoff dates for purchasing prevented planting insurance.

So what does this mean for cattle producers?

Remember the historical relationship – as corn goes up, cattle prices trend downward. It is too early to know whether the 2019 corn crop will be at or below USDA 2019 projected trendline yield (176 bu/acre). Also, in addition to the 2019 corn crop, the global grain pipeline is somewhat full. We still have a large domestic carryover stock, South American production was strong and there is a glut of wheat available. President Trump just announced intentions to implement a 5% tariff on goods imported from Mexico effective June 10. Mexico happens to be the largest export market for US corn.

As summer progresses and crop progress reports come in, the markets will respond accordingly. Corn futures gained 15% in May, have taken a pause as a result of the announcement of tariff intentions for Mexico imports, but are anxiously awaiting the end of the corn planting season and progress reports on the crop.

Beef producers who will wean calves this fall (heavier than normal due to pasture conditions?) are not immune to the corn farmer’s misfortune or issues on the border. If the market response includes higher corn prices, expect feeder cattle prices to soften. If prices that facilitate acceptable profits are available, those averse to risk might consider contracting calves soon for fall delivery. Relative to fall feeder cattle prices, it appears the chance for lower prices outweighs any optimism for a late summer/fall rally.